Collateral Charge Mortgage Vs. Standard Charge Mortgage?

Recently both TD Canada Trust and ING announced that all of their new mortgages will be registered as Collateral Charge Mortgages, and many lenders are expected to follow. In light of the recent announcements, we at CMGC have decided to shed some light on the subject.

First, some background..

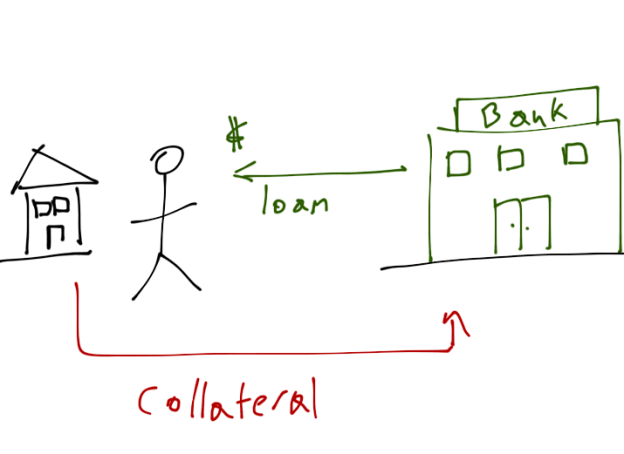

There are two ways to register a mortgage loan. The first being a Standard Charge Mortgage (how most fixed-rate mortgages are being registered) these are done with the Land Title or Registry Office. A Standard Charge Mortgage can be switched, transferred or discharged.

The second being Collateral Charge Mortgage, these are registered under the Personal Property Security Act (PPSA) and can only be discharged, not transferred.

The Collateral Mortgage Explained

Simply put a collateral mortgage is when the lender doubles their security by obtaining BOTH a lien registered against the property and a promissory note.

Unlike the standard charge mortgage, the collateral mortgage is difficult to move to another lender at the end of the term, and costs more to move to another lender. Also, with a collateral mortgage, if you go into arrears or default, the bank has the right to raise your interest rate by up to 10 percentage points. On a debt as large as your mortgage, this could mean a significant charge.

The lender can register a higher property value, up to 125%, so that if you need to borrow money against your equity it can be done quickly for example without any legal fees. This may sound like a good thing, but it is a double edge sword. Basically having the flexibility to borrow increases the time it takes to pay down your mortgage. Also once you register your certain value with your lender the valued amount will not recognized by other lenders.

Another down fall of this type of mortgage is the fact that all of your loans are linked. If for any reason you default on your mortgage the bank can roll any other debts that you have with them, such as a line of credit or credit card debt. This means you can loose your home, and the ability to use those other products as well.

The recent government mandated changes also come into account. Refinances can be done up to 80% of the property value, so if you put down 5% at purchase you are stuck with that current collateral charge mortgage until you pay down your mortgage from 95% of the value to 80%.

Although Collateral Charge Mortgages are not a new thing in Canada, they have been creating buzz within the last couple of months. Mortgage Rates continue at all time lows and locking into a collateral mortgage may not be the best thing for you.

Collateral Mortgages can be tricky, they’re appeal is that you can have access to equity quickly, which is not a good idea if your plan is to pay off your mortgage faster.

At CMGC we are Mississauga’s leading Mortgage Brokers, use our Mortgage Calculator to determine what your options are to obtain the Best Mortgage Rates.